What will have more impact on retirees than the government debt?

(A problem without a solution.)

There is an old joke that’s apropos to today’s financial forecasting:

Two rednecks were returning to shore from a day of fishing. The first one says to the other, “Did you mark the spot where we caught the fish?” The second one says, “Yes, I put an X on the side of the boat.” The first one says, “You Idiot! Next time we may not get the same boat.”

Today’s investors largely are looking for a spot to fish based on what happened in the past hour, day, week or month. Or they make elaborate charts looking for patterns to repeat themselves never asking whether the background of the past results will be anything like the background of the future.

We are facing a tremendous hurdle just trying to overcome $14 trillion national debt, a figure that is increasing every year at a staggering rate because we’re adding more than a trillion dollars every year. $14 trillion divided by a 116 million U.S. households is $120,000 per household.

Unlike business and personal accounting, government accounting does not include unfunded liabilities. These are mind-boggling numbers when accounting for Medicare, Medicaid, Social Security and government pensions. Estimates depend on a discount rate, but including unfunded obligations would bring federal debt north of a half-million dollars per household.

That’s additive to personal debt from mortgages, car loans, credit cards, etc., that well exceed another hundred thousand dollars per household. Those numbers don’t include retirees’ unfunded obligations which are unknown but have to exceed three-hundred thousand dollars per household for long-term-care, and uninsured medical costs, not including provisions for the sandwich generation’s support for elderly parents and adult children in financial difficulties.

All told, federal debt, unfunded federal obligations and personal debt exceed $600,000 per household. Add unfunded personal obligations and we’re talking about almost a million dollars per household for the ever increasing number of elderly.

There are theoretical solutions for these debts and obligations, but few likely practical ones. For example, the government can print money which will bring inflation. Inflation will reduce the apparent size of debts but do nothing for unfunded entitlements indexed to inflation. Getting everyone to cut their body-mass index to 25 and use a vegan diet might reduce uninsured medical costs, but our population has grown too hedonistic for that.

In fact, we’re so hedonistic that we have great difficulty saving money for retirement. It seems more important to live in a large house, have the latest electronics, provide cars for teenagers, and so on, than saving for emergencies, retirement or to accumulate funds for a large future purchase in advance.

The drain of our income for the aforementioned government uses exacerbates the problem. It’s not just our levies for payroll, income taxes and federal taxes on fossil fuels, it’s the innumerable additional taxes, licenses and fees that we get from states and local governments. Indirectly we pay for more taxes as passed on to us by corporations which have to include the cost of their taxes in the products that we buy.

Our aging population means the proportion of workers to elderly will go down, thereby forcing remaining workers to cover an increasing amount of Social Security, Medicare, Medicaid and welfare for the older population. In 2010, the number of those over 65 was 24.6% of those between ages 25 and 65. The Bureau of Economics* estimates that will increase to 36.3% by 2025. Said another way, the elderly will be more of a problem to support by 1.48 times (36.3%/24.6%) in just 15 years! Further, almost 50% of our workers now do not pay any income tax. This problem will grow as more and more workers become unemployed, as lower-income tax credits increase, and as the population ages.

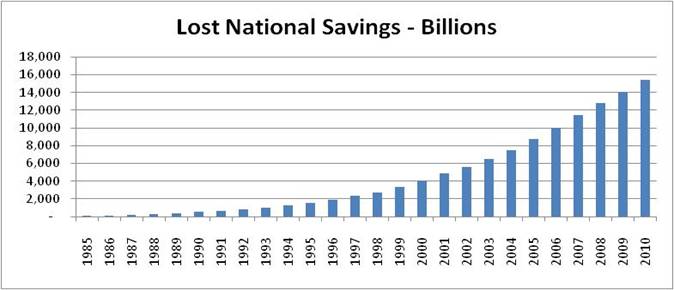

What may be worse than the national debt is the more than $15 trillion of insufficient savings—again, something that printing money won’t help. Printing money will make the savings problem worse because past savings won’t be worth as much, and inflation reduces the real return on which future investment growth depends. This problem may be more important to the over-65-crowd than the national debt because having very little savings to begin with brings early hardship and longer-term inability to survive on nothing but welfare.

Let’s go through the logic behind the $15 trillion savings problem. This analysis does not account for two other major factors which will greatly amplify this problem: (1) The trend away from employee pensions in exchange for employee savings plans, and (2) the aging of our population which will (a) increase the ratio of elderly to the working population by almost 50% in just 15 years, and (b) increase the elderly voting population from 17% in 2010 to 23% in only 15 years* bringing more vocal clamor for larger entitlement programs.

The loss in national savings:

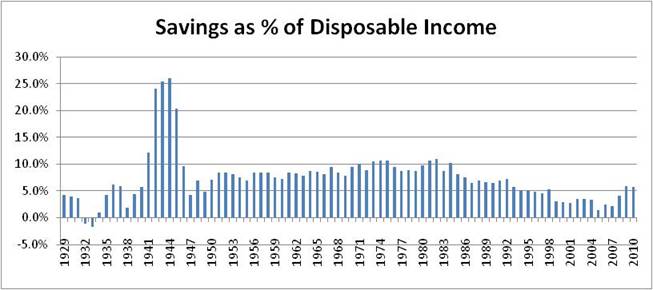

The worst savings we had as a country was during the great depression when savings went slightly negative. The most savings we had on the U.S. record books was over 20% of disposable income during World War II. That was because there was rationing, and, even if not rationed, most goods and services were not available. Virtually all production and services went to supporting the troops, and there was full employment including the national icon, Rosie the riveter. Further, it was patriotic to put money into savings bonds. Even school children saved their pennies to buy savings stamps which could eventually be turned into savings bonds. Saving was the mantra of the time, not today’s consumption.

After World War II, there was a trend to higher savings rates until 1985. Over the period 35 years between 1950 and 1985, the average savings rate was 9%. Together with significant pensions and Social Security, this 9% provided adequate funds for retirement for most people. We should point out, though, average is not the median, which would be somewhat lower. Much of the saving is done by higher income people.

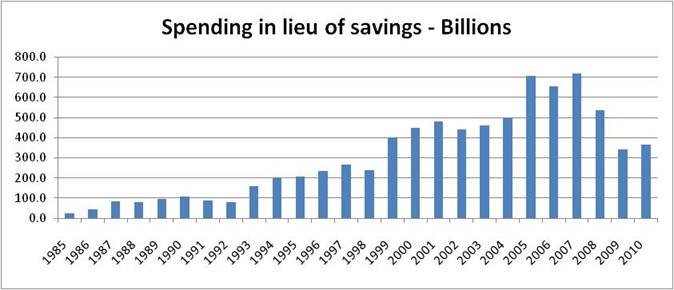

In 1985, we started an expansion of spending that reduced the amount available to save. Consumerism took hold and exploded as people started buying ever larger homes, new automobiles with expensive options, computers, software, audio equipment, ever larger televisions, outfitting their children with their own automobiles, etc. The savings rate declined almost 0.5% each year until 2005 when it briefly went negative for part of the year. Since 2005, savings have increased at an anemic rate.

It’s surprising that people haven’t started to save more now that retirement is in sight for the baby boomers. Almost every financial firm has free retirement planning programs on the Web, but apparently they get scant attention—or otherwise people do an analysis and just give up, assuming that they will muddle by somehow, win a lottery or get support from their kids or the government somehow.

If savings remained at 9% of disposable income, there would be little problem today, but the actual savings had fallen short by a cumulative $15.4 trillion if those savings were invested at 7%.

Catch-up savings required:

So let’s try to find out how much people would have to save over the next 20 years to catch up to the 9% historical saving rate balances. Disposable income was $1.023 trillion in 2010. If there would be no more inflation and people could earn a 7% return, both likely to be highly optimistic, then people would have to save 21% of their disposable income for 20 years to make up for their savings shortfalls from 1985 through 2010.

Practically every assumption above was optimistic in order to get the smallest increase in savings rate. For example, it would be more realistic to assume that people would want to catch up in a lot shorter period of time, and inflation would have made it more difficult. So even with such assumptions, the savings rate would have to go to 21% instantly to regain the lost ground. That effectively requires World War II conditions of absolute minimum consumption—for twenty years!

There is no way that savings can increase that much in so short a time and be sustained for such a long period. It would take government rationing of goods and full employment, just as during World War II. Further, it would require restoration of pensions and no increases in tax or inflation rates. The growth in the number of elderly compared to the number of people employed makes the problem worse.

Let’s face it. As if solving the national debt problem wasn’t bad enough in itself, the impossibility of catching up on lost savings exacerbates our future difficulties. The factors described above cry out for more individual savings while the motivation for savings started disappearing twenty five years ago.

Saving is discouraged by the federal government, businesses and financial firms, all of which want us to spend more to improve the economy momentarily without disclosing, much less quantifying, the penalties that will come in the future.

While the lack of savings will hurt the baby boomers the most initially, the need for additional savings will affect almost every family. We need a whole new culture to reduce spending for individuals and the government as well. We also need higher tax receipts. Our current national debt and people’s lack of accumulated savings are already past the critical stage and beyond recovery. Those individuals that can save substantial amounts and invest successfully in a high government debt situation will be the few that may come close to the kind of retirement previous generations enjoyed. Unfortunately, the majority of people will suffer a greatly reduced standard of living.

We can get a glimpse of the future from Lincoln, CA, where Alana Semuels reports in the Los Angeles Times that “Retirees fill city, not coffers.” The article says, “Lincoln Hills…is one of the fastest growing cities in the state. However commerce is down,…and local stores are closing. Vacancy signs scream from empty storefronts up and down the quaint Main Street…” Look for this to widen as the effects from federal debts, lack of savings and an aging population spread.

Henry K. (Bud) Hebeler, 5/21/11

www.analyzenow.com

* 2011Statistical Abstract, Census Bureau